It’s a bold idea: your favorite shopping app, ride-share platform, or even a gaming service acting like a bank—issuing loans, offering savings tools, or powering real-time payments. This isn’t a hypothetical future. Thanks to embedded finance, it’s already happening. The question now isn’t if every app can become a bank—it’s how soon and what that really means.

As financial infrastructure becomes programmable and pluggable, apps across industries are layering in financial capabilities once exclusive to traditional institutions. This shift is blurring the lines between tech companies and financial providers, giving rise to a new model of “banking everywhere, but not from banks.”

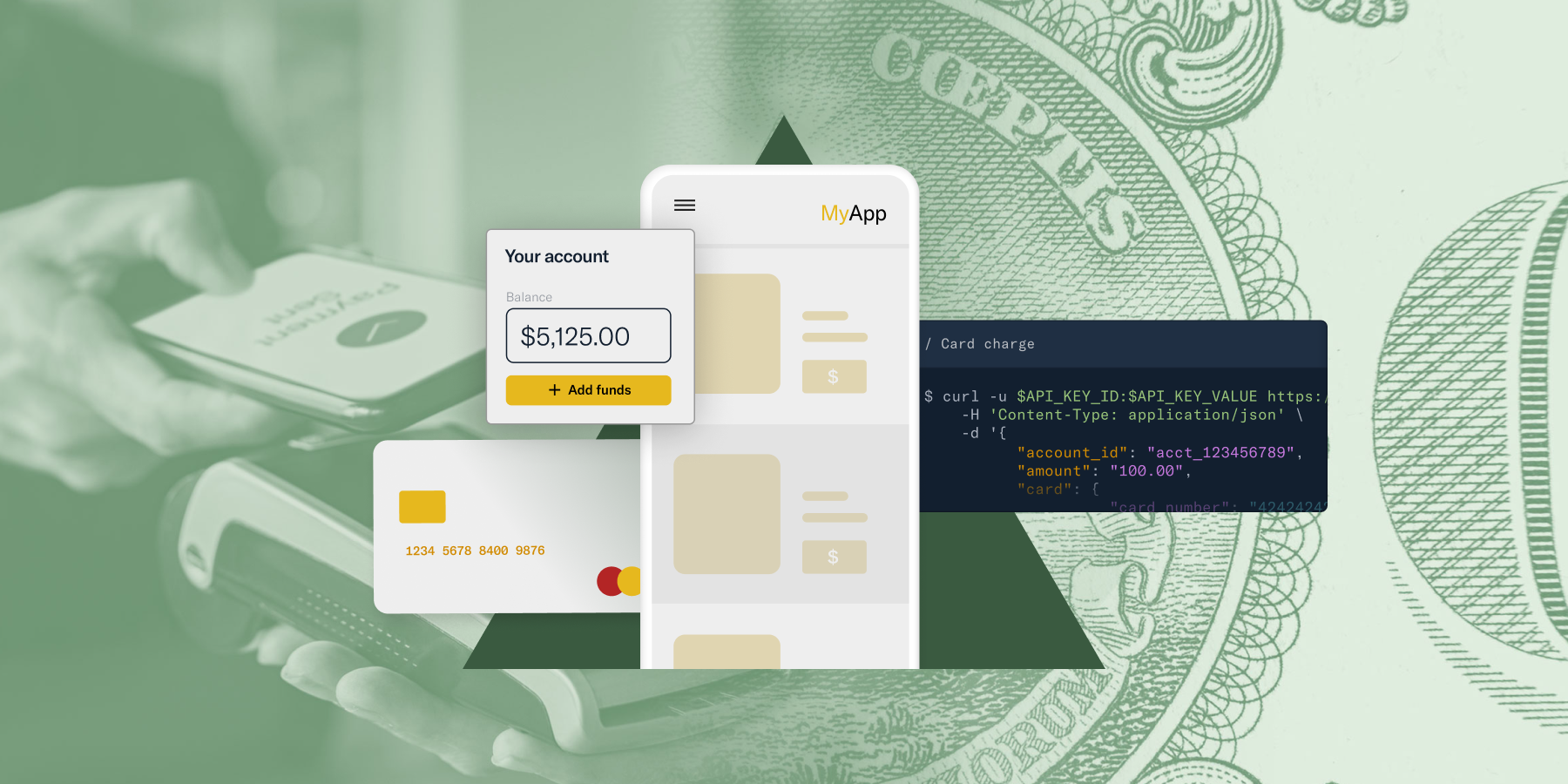

🔹 1. What Is Embedded Finance, Really?

Embedded finance refers to the integration of financial services—such as payments, lending, insurance, and investing—directly into non-financial platforms via APIs and fintech partnerships. Instead of sending users away to a separate bank or app, companies bring the finance directly to the user experience.

For example:

- A small business can get a loan from Shopify without visiting a bank.

- A gig worker can receive instant pay advances from Uber.

- A user can split payments or buy insurance while checking out on an e-commerce app.

Finance, once standalone, is now baked into the flow.

🔹 2. Why Every App Wants to “Be a Bank” (Sort Of)

For platforms, embedding finance isn’t just about convenience—it’s a competitive and strategic move. Offering financial tools:

- Deepens user engagement

- Opens new revenue streams (think interchange fees, lending margins, or insurance commissions)

- Increases stickiness and lifetime value

- Builds trust and loyalty

You don’t have to become a regulated bank—you just embed the functionality, powered by backend fintech providers or licensed financial partners.

🔹 3. Who’s Powering This Behind the Scenes?

The rise of Banking-as-a-Service (BaaS) platforms—like Stripe, Marqeta, Synapse, and Unit—means companies can offer financial features without building infrastructure from scratch or securing banking licenses.

These enablers handle compliance, KYC/AML, fraud protection, and core banking services, allowing tech platforms to focus on user experience and brand differentiation.

🔹 4. What This Means for Traditional Banks

As financial services become a feature—not a product—traditional banks risk being pushed into the background, becoming invisible infrastructure. They may still hold the charters and deposits, but the consumer-facing relationship is owned by the app.

To stay relevant, banks must:

- Embrace platform partnerships

- Offer BaaS themselves

- Reimagine their role as providers of trust, security, and compliance in a more open financial ecosystem

🔹 5. Risks, Regulation, and the Fine Print

While the opportunities are vast, there are serious considerations:

- Regulatory clarity is still evolving—especially around consumer protections, data use, and liability in embedded financial products.

- Trust and transparency must be preserved. Consumers may not always realize they’re engaging with financial services through a third party.

- Tech companies must ensure financial literacy and risk disclosure, especially with lending, investing, or BNPL offerings.

Embedded finance brings power—but also responsibility.

Conclusion: A Financial Future Without Banks—or Just Without Bank Branches?

So, can embedded finance turn every app into a bank? Functionally, yes. Legally and ethically, it’s more complicated. What’s clear is that financial services are becoming omnipresent, invisible, and deeply integrated into our digital lives.

The future of banking may not be one monolithic institution—it may be dozens of apps, each offering the exact financial tool you need, right when you need it. It won’t look like a bank. But it will work like one.